For institutions specializing in mortgages, personal loans, or commercial lending, success hinges on efficiency, compliance, and maintaining a transparent, empathetic client journey.

In this guide, you will understand what a lending CRM is, how it differs from a Loan Origination System (LOS), key features to look for, and how it supports each stage of the loan lifecycle.

What is a lending CRM?

Unlike generic CRMs, a lending CRM is built around compliance-heavy, document-driven, and time-sensitive lending workflows.

Lending CRM vs Loan origination System (LOS)

A Lending CRM manages:

- Lead capture

- Borrower communication

- Relationship history

- Workflow orchestration

A LOS (Loan Origination System) handles:

- Underwriting

- Credit rules

- Decisioning

- Disbursal logic

Key features to look for in a lending CRM

Loan Origination Automation

- Digital forms: Borrowers fill applications online instead of manual. Data flows directly into CRM/LOS to eliminate errors.

- Application capture: Captures loan requests from multiple channels - website, agents, partners, branches - into one dashboard for faster follow-ups.

- Lead-to-loan workflows: Workflows are pre-built that guide each borrower from one step to the next.

- Auto-assigned tasks: Automatically assigns work (document collection, calls, verification) to the right team or agent based on rules, region, or availability.

Automated KYC/AML Checks

- Pan/Aadhaar verification: Instant verification via government APIs to confirm identity, age, and consistency of details.

- Address verification: Digital verification through utility data, geo-tagging, or bureau checks, reducing physical verification needs.

- Anti-fraud checks: Flags suspicious pattern, for example, mismatched documents, fake ID, or high risk submissions using AI.

Credit Risk Assessment Tools

- Scorecards: Evaluates borrower’s creditworthiness by assigning scores on various factors (income, credit history, DTI ratio).

- Bank statement analyser: Analyze borrower’s 6-12 months of bank statement to detect income patterns, cash flow, salary credits, and financial stress.

- Income validation: Cross-checks claimed income with statements, GST data, or bureau data to ensure eligibility.

- In-app credit bureau integration: Pulls CIBIL/Experian reports directly into the CRM, removing manual downloads and uploads.

Document Upload & Management

- Borrower portal: Dedicated portal to upload required documents eliminating manual form submissions and bank visits.

- E-signatures: Enables digital signing of loan agreements to speed up sanctioning and disbursal.

- Auto extraction (OCR): Extracts data from PAN, AADHAR and other documents without manual intervention.

Underwriting Workflows

- Approval hierarchy: To ensure consistency, guides underwriters through rule-based checks, exceptions, and final approvals.

- Decision logs: Maintains a traceable log of who approved what and why for compliance and audit.

- Automated conditions: Applies conditional approvals, for example, “Need additional proof” and notifies the borrower automatically.

Loan Disbursement Tracking

- Payout status: Lender’s portal shows the loan stages (disbursed, pending or failed)

- Repayment schedules: Auto-generates repayment plans and syncs them with the borrower’s communication reminders.

- Collection reminders: Nudges for upcoming EMIs, pending dues, and overdue accounts.

Compliance Reporting & Audit Trails

- RBI requirements: Supports data retention, audit-ready logs, KYC compliance, and fair practice code workflows.

- Logs of approvals: Every decision, timestamp and user activity is tracked.

- Secure data storage: All stored data is encrypted and given access control to meet BFSI security standards.

Communication Automation

- WhatsApp reminders: Automated reminders for document submission, KYC completion, approvals, and EMI reminders.

- Email + SMS templates: Uses pre-built templates to send email/SMS for approvals, rejections, pending tasks, and status updates.

- Application status updates: Borrowers receive timely updates on their application stage without manual visits/calls.

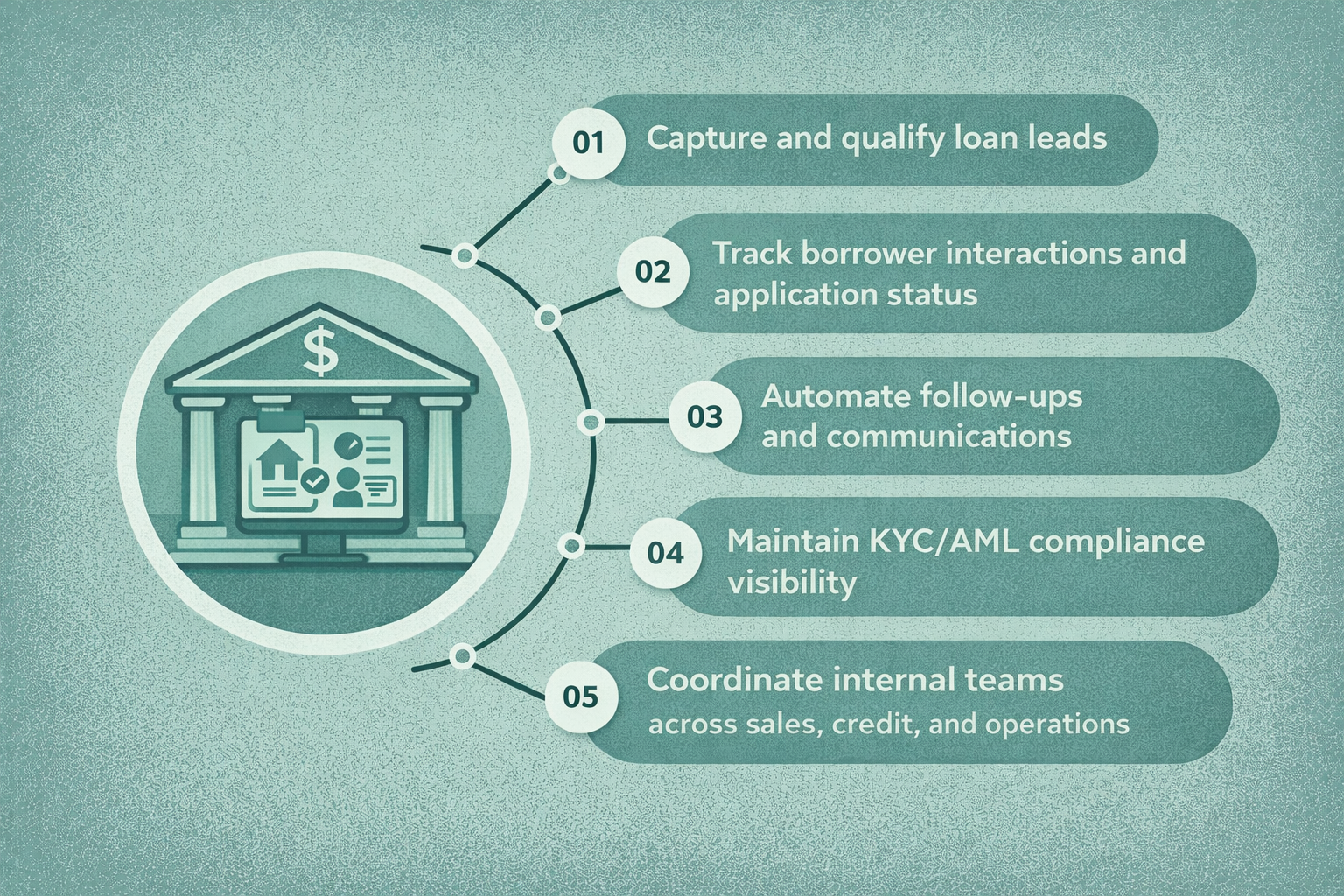

Role of lending CRM across the loan lifecycle

Lead Capture → Auto-qualification

All leads, whether it came from SEO, paid ads, or referrals, are captured. The CRM assigns points based on behavioural (e.g., opened the loan calculator on the website twice) and demographic (e.g., location, stated income) data, sending the low-scoring leads into a nurturing sequence of automated emails or SMS.

KYC/AML Validation

Prospect uploads documents (ID, proof of income) directly into the CRM portal. The CRM then uses APIs (Application Programming Interfaces) to connect with external servers for instant verification of KYC and screening against AML.

This reduces drop out rate and the physical back-and forth.

Underwriting Decisions Faster

Even when underwriting is handled in an LOS, the CRM provides visibility and communication continuity, allowing loan officers to quickly request clarifications or documents.

Loan Sanction & Disbursement

Once approved, the system generates an offer letter with correct terms and interest rate.

The unified workflow ensures that when the borrower digitally signs (e-signature integration), the system will create a loan account in the Core Banking System (CBS), triggering the disbursement of funds, largely reducing human error that could cause delay in funding.

Collection Automation

The CRM tracks the payment schedule and uses predictive analytics to identify potential defaults early before they miss a payment (churn prediction).

The ‘Collection Automation’ then triggers scheduled, personalized payment reminders via the customer's preferred channel (SMS, email, WhatsApp) a few days before the due date. This proactive approach significantly reduces delinquency rates and the need for costly manual collections.

Benefits of a Lending CRM

- Shorter turnaround time (TAT)

- Higher application completion rates

- Improved compliance visibility

- Lower operational costs

- Better borrower experience

How to choose the right lending CRM

Answer these questions before you decide on implementing a CRM:

- Is it scalable as loan volumes grow?

- Does it integrate easily with LOS, bureaus, and core banking systems?

- Is it easy for field agents and ops teams to use?

- Does it meet RBI and BFSI security standards?

- Can workflows be customized to your loan products?

Choosing the right lending CRM like Superleap moves you from simply tracking data to actively managing the risk, efficiency, and customer experience necessary to scale your lending business successfully.

.jpg)

.svg)

.svg)

.svg)

.svg)